Structuring a Business Sale to Minimize Taxes: Asset vs. Stock Sales

When selling your business, transactions take two general forms. These are asset sales and stock sales.

How you decide to structure your business sale will have significant tax implications on your eventual exit. While a certain form may benefit the seller, there are reasons that the buyer may prefer the opposite method. Unfortunately, it’s not completely up to you; however, understanding the nuances of each option is vital for maximizing both your sales price and your after-tax return. Understanding how asset sales and stock sales work is a basic requirement of crafting an optimal business exit strategy.

Key Takeaways

- Asset sales typically favor buyers

- Stock sales generally provide better tax treatment for sellers

- Your business industry can dramatically impact which structure works best

Prefer to watch a video? Check out our YouTube here.

Understanding the Difference Between Asset and Stock Sales

Depending on the type of business you run, an asset sale and stock sale can result in significantly different outcomes and scenarios.

In an asset sale, the buyer purchases the underlying assets of your company, transfers them to their company, and you continue to own what is left of your company. There are two main reasons that buyers do this. First, they don’t retain the liabilities that you incurred and are attached to your old company. Essentially, and as always there are exceptions, they get a fresh start. Second, they can utilize depreciation to reduce their taxes in the early years of ownership, especially related to fixed assets like equipment, which can receive bonus depreciation.

In a stock sale, the buyer purchases the equity of your company and continues to run your business as it is currently constituted. In this scenario, you are selling the ownership interests in your company itself. The buyer, meanwhile, assumes all previous liabilities associated with the company and does not receive the improved tax basis on the underlying assets unless certain elections are made.

Tax Implications for Sellers

As a seller, it’s important to know how your assets are treated for tax purposes. In an asset sale, the purchase price will be allocated amongst the assets the business owns. This means that you could owe ordinary income taxes or depreciation recapture on a portion of your sale. If you were expecting capital gains, you could be in for a rude awakening. Generally, asset sales are less favorable for the seller and more favorable for the buyer.

If you have a significant amount of equipment or real estate that you have depreciated, you will also owe depreciation recapture taxes. Section 1245 property is subject to ordinary income taxes and Section 1250 property is subject to a mixture of ordinary income and capital gains. These rules are Section 1245 and 1250 recapture rules and you should review if you have any assets subject to depreciation recapture before you sell.

In a stock sale, almost all of this goes out the window and you only need to worry about your basis against the sales price. Your capital gains are subject to capital gains taxes, and while you will owe capital gains taxes, the highest capital gains rate of 20% sure sounds a lot better than the highest ordinary income rate of 37%. Another thing to consider is the Qualified Small Business Stock Exclusion or QSBS. The QSBS Exclusion excludes up to $15m or 10x your investment amount from capital gains if you meet certain parameters. This only applies to stock sales, although certain types of liquidations may also be eligible.

Another factor to consider would be your state’s individual taxes. Most taxes for states are equalized for capital gains and income taxes. In Georgia, both your capital gains and income are subject to the same 5.29%. However, in Washington there is no ordinary income tax but a 7% capital gains tax once you reach certain levels. These differences could wind up changing your preference, so keep an eye on them!

All in all, a stock sale is generally preferred for a seller. However, asset sales can be called for in certain industries and deals. You may also be able to negotiate a higher overall purchase price to account for having to do an asset sale, so don’t obsess over executing a stock sale at all costs. Remember, taxes aren’t siloed and it’s all part of one larger deal, which makes Ironclad exit planning essential.

Tax Implications for Buyers

If you’re considering buying a business, then you’re naturally on the opposite side of the table from sellers. Whereas a seller may prefer a stock sale, a buyer may prefer an asset sale. The main reason for this is how the purchase price allocation works and its impact on depreciation.

In a stock sale, a buyer amortizes their purchase price over 15 years. In a $10,000,000 purchase this means you would receive $666,666.67 in annual amortization.

In an asset sale, if that same business has bonus depreciation eligible equipment worth $5,000,000, the purchaser would be in line for $5,000,000 of year 1 deductions (bonus depreciation at 100% is back with the OBBBA) and $333,333.34 in annual amortization. These additional early-year deductions could help a buyer during the early years of trying to manage their new acquisition’s cash flow.

In some cases where a stock sale is desired, you can also make a Section 338(h)(10) election. This election allows you to have your stock sale treated as an asset sale for tax purposes. It requires both parties to agree but can allow additional tax planning flexibility.

All in all, an asset sale is generally preferred for a buyer. As I said earlier, remember this is all part of a larger deal and shouldn’t be looked at on its own.

Is an Asset Sale or Stock Sale Better?

Your business is unique and that means that your sale will have its own characteristics that need to be planned for. At Ironclad Wealth Management, we will never say that one option is always best because that’s an impossible generalization to make. I find that the easiest way to think of the difference in asset and stock sales is to use an example.

Imagine you’re a financial planning firm or another professional services firm. In all likelihood, your business is made up of your personal professional expertise, your staff’s expertise (which you bill on), your reputation, and your client relationships. You may also have some desks, chairs, computers and other items, but these would be a small portion of what a buyer would be purchasing.

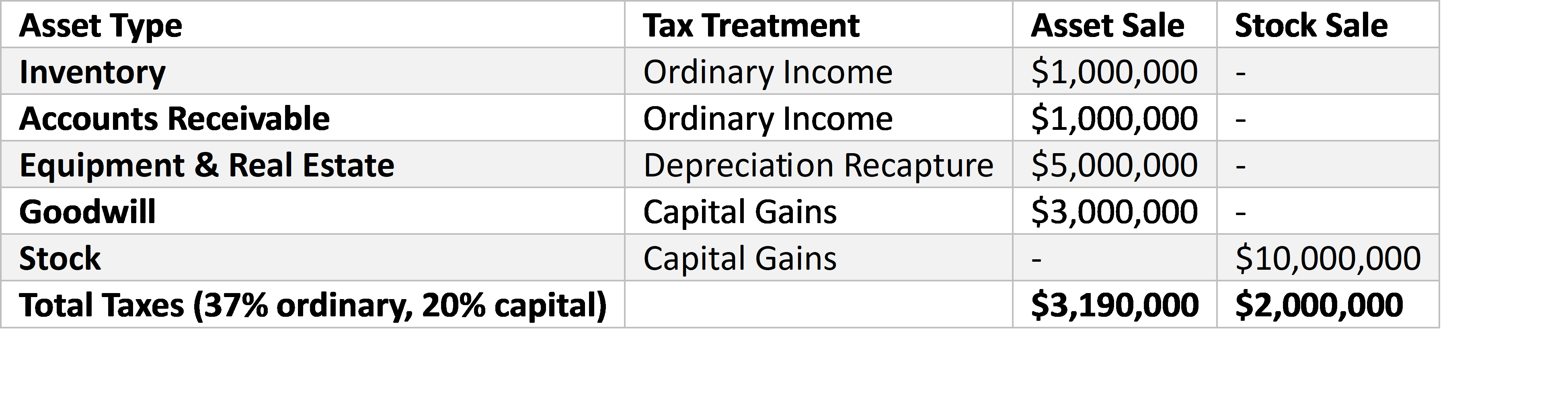

Here’s how an asset sale and stock sale may differ for this business if it sold for $10,000,000:

As you can see in this example, there are minimal business assets. As a result, there is a minimal difference in tax treatment. So really, you can argue about tax treatment and negotiate, but other considerations will most likely take precedence over the tax implications.

However, imagine you own a business that produces goods, and you own your own factory. Then what is a buyer purchasing? They are purchasing your reputation, but they may also be purchasing your accounts receivable, your inventory, and your factory. That could be a majority of the purchase price, which could result in a huge difference!

As you can see, in this case the difference is $1,190,000 in taxes when choosing to utilize an asset sale vs. stock sale. In this example, that is because inventory and accounts receivable are non-capital assets, meaning that they’re taxed at ordinary income rates. All of the sudden, asset vs. stock sale considerations skyrocket in importance. Imagine what would happen if you just listened to your buyer and didn’t review the tax considerations from your perspective? You would wind up with a substantially higher tax bill than you projected, possibly changing your retirement plans and meaning you can’t close your Wealth Gap.

So, which is better? It depends on the deal. Generally, buyers prefer asset sales, but sellers prefer stock sales. However, every deal has different facts and requirements and should be analyzed on a case-by-case basis.

Summary

Your business sale tax strategy shouldn't be an afterthought. The difference between asset and stock sales can easily reach seven figures in additional taxes, but the "better" option depends on your specific situation. Professional business exit strategy planning before you enter serious negotiations can save substantial taxes and help you negotiate from a position of knowledge rather than hoping for the best.

Remember: buyers and sellers have naturally opposing preferences on sale structure, but creative planning and negotiation can often find solutions that work for both parties.

Ready to optimize your business sale strategy?

Ironclad Wealth Management specializes in business sale tax planning for small business owners. We help you model different sale structures, optimize for taxes, and coordinate with your entire professional team to maximize your after-tax proceeds.

Before you sign your LOI, let's ensure you're structuring your sale for maximum tax efficiency.

Schedule a business exit planning consultation to discuss your specific situation and explore tax-efficient sale structures.

Want to Keep Reading more about saving capital gains on your business sale? Check out our blogs on:

- Ultimate Guide to Saving Taxes when Selling a Business: Hub Page

- Installment Sales

- Structured Installment Sales

- Qualified Opportunity Zone Funds

- Tax Loss Harvesting

- Charitable Remainder Trusts

- Employee Stock Ownership Plans (ESOPs)

- Qualified Small Business Stock Exclusions (QSBS)

One Seven LLC ("OneSeven") is a registered investment adviser with the U.S. Securities and Exchange Commission (SEC). Registration with the SEC does not imply a certain level of skill or training. All titles listed for individuals associated with Ironclad Wealth Management represent the individual's role with Ironclad Wealth Management, and not their role with OneSeven. Services are provided under the name Ironclad Wealth Management, a DBA of OneSeven. Investment products are not FDIC insured, offer no bank guarantee, and may lose value. Please visit our websitewww.WeAreOneSeven.com for important disclosures.

Please note, the information provided in this presentation is for informational purposes only and investors should determine for themselves whether a particular service or product is suitable for their investment needs. Please refer to the disclosure and offering documents for further information concerning specific products or services.

Nothing provided in this presentation constitutes tax advice. Individuals should seek the advice of their own tax advisor for specific information regarding tax consequences of investments. Investments in securities entail risk and are not suitable for all investors. This site is not a recommendation nor an offer to sell (or solicitation of an offer to buy) securities in the United States or in any other jurisdiction.